Healthcare Startups take too long to go to market hence innovations do not get to the American people in a form and fashion conducive to the aims of healthcare quality and performance in population health management.

When I left my management role at Humana to enter into the startup world, I was shocked to find that a vast majority of Health Tech organizations are founded by innovators with non-healthcare backgrounds.

Healthcare Startups take too long to go to market hence innovations do not get to the American people in a form and fashion conducive to the aims of healthcare quality and performance in population health management.

When I left my management role at Humana to enter into the startup world, I was shocked to find that a vast majority of Health Tech organizations are founded by innovators with non-healthcare backgrounds.

I found that, in my conversations with startup leaders, they were overconfident and naive about the industry; about the many roadblocks and nuances of running a successful healthcare operation (ie. ‘Regulation Nation’, business complexity, and long ‘sales’ cycles become blockers to market entry).

Sadly and ultimately, this dynamic ‘kills’ otherwise life-changing innovations. We find this to be unfair. Not only to the startup but to the People. To you, Don. To me and my loved ones. These incredible inventions and ‘innovations’: dead on arrival; attributable to the founders’ lack of healthcare business navigational competency and expertise.

Educating the leaders was my first instinct (see me in action: Managed Care 101: Boot-camp for Healthcare Entrepreneurs).

Then, Carenodes Accelerator was born: a program along with outcomes not seen in the country. Programmatically, we provide an integrated suite of advisory, technological, data, clinical, and operational capabilities to ‘jumpstart’, or power, the startup on day 1.

We signed our first health technology startup in August 2020. Today, Carenodes has grown to 7 portfolio digital health startups. We are 100% fiscally self-sustained, fully bootstrapped, and led by a majority ‘minority’ team. Our leadership and downstream team composition is what the ‘equity and diversity’ movements of modern-day fantasize about.

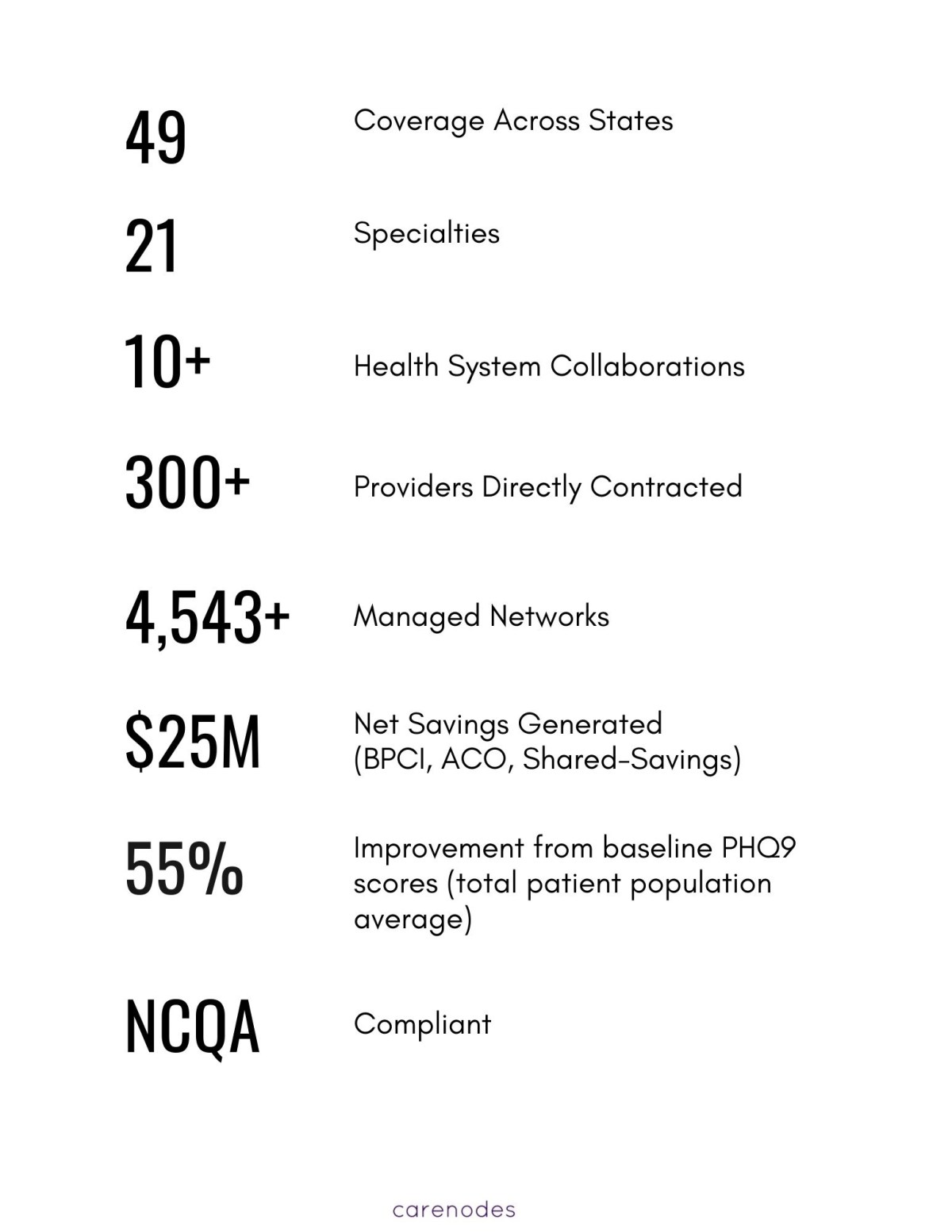

As of the time of this correspondence, our startup medical groups have raised an aggregate of $210M in funding.

We have, in aggregate, provided 96,637 appointments to 36,718 patients (2019 – 2022) in 50 states + DC. We have accelerated Digital healthcare innovations to a scale now reaching 48 million Americans.

Net result on the US Healthcare System is: Access. Access for Payer, Provider & Patient. Not just one of these ‘nodes’ — but all.

By becoming ‘in-network’, the out-of-pocket burden for offerings based on ‘cash only’ direct-to-consumer strategies is reduced tremendously making it affordable for the consumer. At the same time, our digital health organizations generate (much) greater revenue by billing insurance and coordinating care in a way that is not incentivized in a cash-only model. Our medical group startups generate revenues in 6 months via health insurance network participation.

We provide a robust operation with clinical oversight beyond just ‘being an app’ on a cash model. Payers feel more comfortable with that type of organization. Hospitals and health systems trust the expertise and buy-in. Especially since insurance will be paying for the services.

This has benefited the startup, the patient, the payer, and us — the regular folks who NEED access.

What is our impact? See the following outcomes and have these figures speak for themselves:

Carenodes real-world implications and outcomes (from Oct 1, 2019 – Jan 1, 2022):

- Using patented IoT-connected socks, we avoid 91% of all diabetic foot ulcer amputations.

- Using FDA-approved AI technology, we monitor the hearts of CHF/HF (heart failure) patients at home and at skilled nursing facilities in NY and CA. Diverting 75% of avoidable ER utilization.

- Using our 24/7 access to care platform, we have provided 66,467 virtual opioid use disorder treatment appointments.

- Using our Biopsychosocial Network, we extend a highly coordinated ‘plug & play’ provider network of 134 health providers (and growing) to help ease the major challenges of workforce supply, recruitment, and management.

- In connection with UCI and other major health systems, we are one of the very few delivery organizations providing Hospital at Home.

- We have, in aggregate, provided 96,637 appointments to 36,718 patients (2019 – 2022) in 50 states + DC. We have accelerated Digital healthcare innovations to a scale now reaching 48 million Americans.

Here is a one-minute video update of our organizational position opening in the year 2022 (this clip is not made searchable on YouTube, but you should have access with the link).