This blog post delves into the complex challenges facing the health insurance industry in 2025, a year poised to be a pivotal moment for insurers, particularly those heavily invested in Medicare Advantage plans. Rising healthcare costs, increased patient demand, and heightened government scrutiny are converging to create what we’re calling a “perfect storm.” This confluence of factors threatens profitability and necessitates a critical reevaluation of existing operational strategies. This post expands on the themes discussed in our latest podcast episode, exploring these challenges in greater depth and offering insights into potential solutions for both insurers and healthcare providers.

Rising Healthcare Costs: A Looming Crisis

The escalating cost of healthcare is arguably the most significant challenge facing insurers. Inflation, technological advancements, and the increasing complexity of medical treatments all contribute to this unsustainable upward trend. The post-COVID surge in patient utilization, with many seeking deferred procedures, has exacerbated the problem, placing immense pressure on insurers’ financial reserves. This increased demand is straining existing resources and impacting profitability, pushing medical loss ratios (MLRs) higher than ever before. The implications are profound, forcing insurers to re-evaluate pricing strategies, negotiate more effectively with providers, and explore innovative cost-containment measures.

The Impact on Medicare Advantage

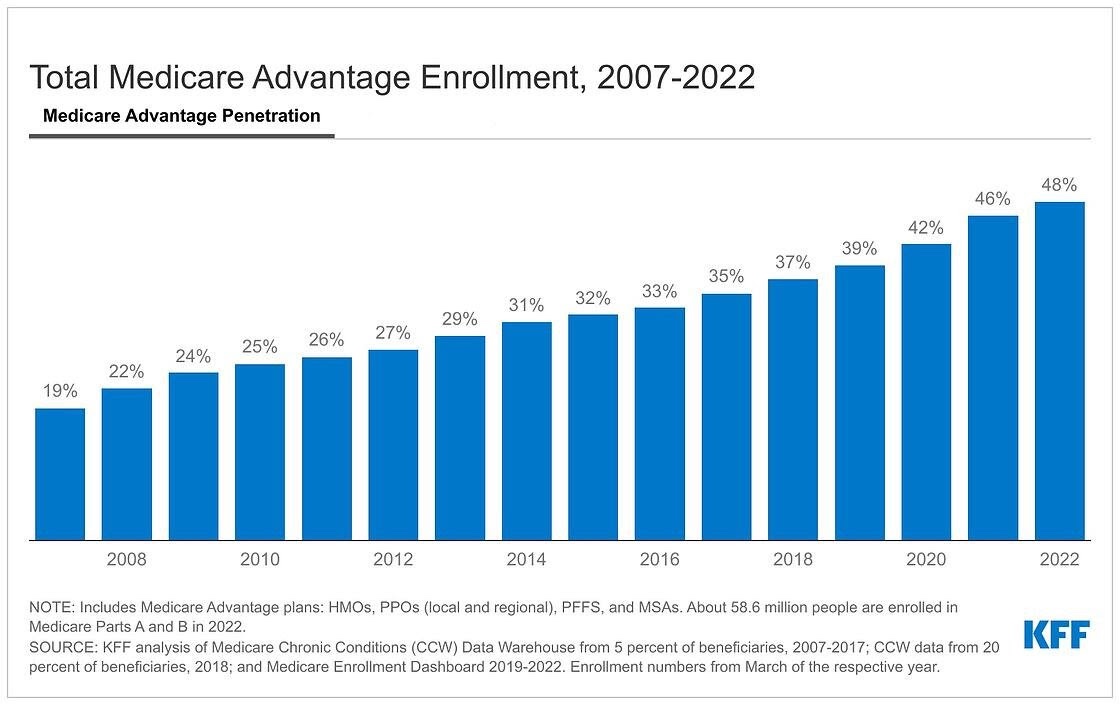

Medicare Advantage (MA) plans, once considered a goldmine for insurers, are particularly vulnerable in this environment. The increased demand for MA plans, coupled with rising healthcare costs, is squeezing profit margins. Major players like Humana and UnitedHealth Group, heavily reliant on MA for revenue, are grappling with these challenges head-on. Their financial performance is becoming increasingly dependent on their ability to manage costs efficiently while maintaining patient satisfaction and adherence to regulatory requirements.

Increased Patient Demand: A Double-Edged Sword

While increased patient demand initially appears beneficial, in the context of rising costs, it becomes a major challenge. Insurers are faced with a difficult balancing act: fulfilling the needs of a growing patient population while simultaneously controlling costs and maintaining profitability. This necessitates a shift towards more proactive and personalized care models that prioritize preventative measures and disease management. Strategic partnerships with providers are crucial for achieving these goals.

The Need for Personalized Care

The sheer volume of patients requires a move beyond traditional, reactive models of care. Personalized care, driven by data analysis and predictive modeling, is becoming essential for identifying high-risk individuals and implementing targeted interventions. This approach not only improves patient outcomes but also helps to manage healthcare costs more effectively, ultimately impacting the MLR and safeguarding insurer profitability.

Increased Government Scrutiny: Navigating Regulatory Hurdles

The health insurance industry is facing unprecedented levels of government scrutiny. Lawmakers are increasingly focused on issues of transparency, affordability, and access to care. This heightened scrutiny translates into stricter regulations, increased audits, and potential penalties for non-compliance. Insurers must navigate this complex regulatory landscape while ensuring they maintain ethical and transparent practices.

Adapting to Regulatory Changes

The regulatory environment is constantly evolving, requiring insurers to be adaptable and proactive. Staying informed about new regulations, investing in compliance programs, and engaging with policymakers are crucial for navigating this challenging landscape. Failure to adapt could lead to significant financial penalties and reputational damage.

Opportunities Amidst the Storm

While the challenges are significant, the current climate also presents opportunities for innovation and growth. Entrepreneurs and healthcare providers can leverage this disruption by focusing on high-cost patient areas and developing innovative solutions that improve efficiency and reduce waste within the healthcare system. New models of care, such as value-based care, offer potential avenues for both improved patient outcomes and reduced costs.

Innovation in Healthcare Delivery

The need for cost-effective and efficient healthcare delivery models has never been greater. Entrepreneurs are stepping up to the plate, developing innovative technologies and solutions to address these challenges. These range from telehealth platforms and remote monitoring devices to AI-powered diagnostic tools and personalized treatment plans. Insurers that embrace these innovations and forge strategic partnerships with these innovators will be better positioned to thrive in the evolving healthcare landscape.

Conclusion

The healthcare industry in 2025 faces a perfect storm of rising costs, increasing patient demand, and intensified regulatory scrutiny. Insurers, especially those heavily reliant on Medicare Advantage, are experiencing significant financial pressure. This necessitates a complete re-evaluation of operational strategies, focusing on cost containment, personalized care, and proactive compliance. However, amidst these challenges lie significant opportunities for innovation and growth. By embracing new technologies, fostering strategic partnerships, and prioritizing patient-centric care models, both insurers and healthcare providers can navigate this turbulent environment and emerge stronger. To delve deeper into this topic and explore potential opportunities, please listen to our podcast episode, “2025 Opportunities in Healthcare: Navigating the Perfect Storm.” This episode provides further insights into the challenges and opportunities discussed in this blog post and offers actionable strategies for navigating the complexities of the 2025 healthcare landscape.

Companies mentioned in this episode:

Research Links:

- There’s uncertainty ahead for the health insurance industry in 2025

- Hearing: Hacking America’s Health Care: Assessing the Change Healthcare Cyber Attack and What’s Next | The United States Senate Committee on Finance

- Potential Health Policy Administrative Actions in the Second Trump Administration | KFF

- UnitedHealthcare Profits Less About Denials, More About The Pandemic

- Higher and Faster Growing Spending Per Medicare Advantage Enrollee Adds to Medicare’s Solvency and Affordability Challenges | KFF

- Humana stock declines on Medicare Advantage star rating struggle | STAT

The Definitive Playbook for Choosing Behavioral Health Markets – Value Based Care Advisory (VBCA) Podcast

- The Definitive Playbook for Choosing Behavioral Health Markets

- Medicare Negotiates Like an Owner. Commercial Doesn’t.

- The Rural Health Transformation Fund: What States Are Funding in 2026

- Medicare Advantage 2026: How Payers Are Choosing Partners

- Digital Health at a Crossroads: The Fallout from a $100M Adderall Fraud Scheme